There are tons of Investment Bankers right from bulge brackets (read Goldman Sachs, JP Morgan, Morgan Stanley) to small ones (ones with 2 – 3 people) who provide their services in Private Equity. While the bulge bracket will not do deals below USD 100 million, the others also have some sort of minimum deal size they target at to report a minimum revenue per deal to cover their cost and expenses per month.

There are tons of Investment Bankers right from bulge brackets (read Goldman Sachs, JP Morgan, Morgan Stanley) to small ones (ones with 2 – 3 people) who provide their services in Private Equity. While the bulge bracket will not do deals below USD 100 million, the others also have some sort of minimum deal size they target at to report a minimum revenue per deal to cover their cost and expenses per month.

In our experience, most of the start-up Clients, we have worked with, need some sort of consulting (especially for a 5-year strategic plan) before pitching the idea to investors. This consulting, in our opinion, is essential to ensure your business idea and business model is in sync with the business strategy, the financial projections (also known as financial model), the market trends and the competitive forces/analysis. These 6 parts form the major ones from the business idea perspective.

Market segment (and market trends) plays a major role because you will operate and grow within it (remember, B2B and B2C segments have different business dynamics with its own cost and revenue drivers. Because of this, investors evaluate them deeply from at least 5 years down the line. Off late, Robotics in India, for example, is doing well. So, Investors would explore the market for it, your idea to address and tap the market, the team and the initial traction).

However, we should keep in mind that an Investor always invest in the Entrepreneur – it is s/he who converts the business idea into a tangible sustainable business and give the investor a successful exit. Hence, a credible team goes by far to attract investors and get funded.

For example, an e-commerce business, at the core, should have a CEO (sales), COO (operations) and CTO (technology). The core team may be surrounded by Advisors of respective fields to help them formulate business plan and make strategic decision. We have seen most successful businesses with this structure. As and when you grow, a CFO needs to be present in the core team.

Whether investors would like to see traction at the initial stage depends on the idea, its stage and the investor’s investment philosophy. For example, there are technology companies that gets funded even at idea stage (the company is not on the ground yet). Such cases require a strong large untapped market, commendable business plan, sustainable and scale-able business model and a strong team. B2B businesses are not highly scale-able (at least to the best of my knowledge), but usually have steady cash flow after 3 years, especially once they win large / long-term contractual agreements.

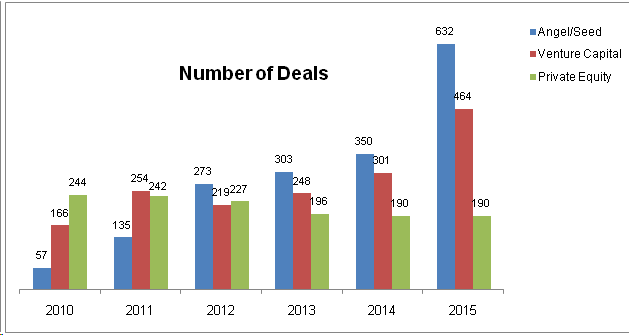

Ideally, an angel investment takes 75–90 days, and a VC round 4 – 6 months (first discussion to receiving the money into your bank account). This is assuming that your information memorandum is ready. Once invested, an angel investor would stay invested ideally for 3 years on an average and exit with 2x – 4x returns, and a VC stays invested up to 7 years (depends on the fund) and exit with up to 10x returns. For example, Tiger Global, one of the top VC investors, is estimated to make a partial exit from Flipkart with 3x return; EVC Ventures, an early-stage VC fund, exited from Milkbasket with 200% IRR of their initial investment.

Our story: Let me introduce you to Garg Partners

![]() Garg Partners is a management consulting and investment banking firm dedicated to helping start-ups, small and mid-size enterprises improve organizational performance and with private equity and M&A advisory.

Garg Partners is a management consulting and investment banking firm dedicated to helping start-ups, small and mid-size enterprises improve organizational performance and with private equity and M&A advisory.

In the last 3 years, Garg Partners helped (pre-revenue) start-ups, high-growth and distressed businesses across 13 industry verticals (retail & e-commerce, manufacturing, logistics, travel & transport, food & beverages, fashion & apparel, automotive, specialty chemicals, engineering, technology, media, bio-technology and healthcare) develop 5-year strategic plan, improve organizational performance (operational efficiency, sales, inventory, gross margin, EBITDA/EBIT margin, cash flow and profitability), develop marketing and branding strategy (including celebrity brand endorsement), initiate strategic partnerships, restructure organization, restructure debt and originate strategic M&A transactions. We had built investor-facing pitch-deck and 5-year financial model for 43 products and 19 countries with manufacturing plant and R&D facility for raising equity capital, constructed accretion/dilution analysis for buy-side M&A (51% stake acquisition with 25% cash and 75% stock), calculated the market size for 75 products, designed CEO compensation, prepared numerous pitch-decks and financial models for sell-side M&A and performed valuations, besides various corporate advisory projects.

Over the past 5 years, Garg Partners has built relationship and understood the investment philosophy of 450+ Private Equity and Venture Capitalists (incubator, accelerator, seed, early-stage, growth and buyout) across India, Hong Kong, Singapore and USA, 340 accredited Angel Investors and 10 large business houses in India for strategic minority investments.

In FY19, Garg Partners clocked a growth of 313% by revenue and 100% by new Client acquisition over FY18. Reference Client base grew 60% over the last year and contributed 39% to FY19 revenue. This year’s performance is followed by a revenue growth of 46% in FY20 and 23% in FY21.

Write to me: nitin@gargfinanceblog.com

Last week, one of my e-Commerce Clients in the B2C segment asked me this question: “Where can I register my company, other than in India? Is Singapore a good option?”

Last week, one of my e-Commerce Clients in the B2C segment asked me this question: “Where can I register my company, other than in India? Is Singapore a good option?”