Angel and Venture Capital investment set a new stage in Year 2015, both in value and volume, which in effect drove the overall private investments to a new high

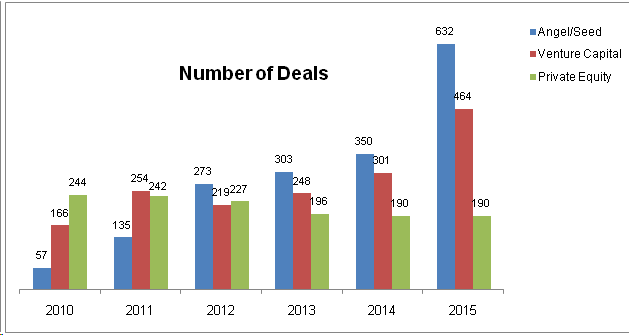

According to VCCEdge, Angel and VC investors closed a total of 1,096 deals in 2015, an increase of 68% from last year, a record jump and also the highest early-stage investment in India. Of these, angel and seed investors funded 632 deals, whereas VCs closed the remaining.

In value terms, angel and VC firms together contributed 24.5% of the total private investments in 2015, a growth of 17.2% as compared to last year. On a standalone basis, angel funding crossed US$ 300 million for the first time, an increase of nearly 60%, from US$ 196 million in 2014,. VC funding showed a similar trend, clocking deals worth US$ 5.183 billion, a growth of nearly 127%, as against US$ 2.287 billion last year.

Year 2015 also witnessed highest funding in eCommerce and Technology industries. According to Padmaja Ruparel, President, Indian Angel Network “The technology and e-commerce sectors have been in the limelight in 2015, and our country is the fastest-growing start-up ecosystem in the world, right now. 11 of the 68 ‘unicorns’ globally, (companies that are valued at over US$ 1 billion) are of Indian origin.”

Currently, India is home to over 18,000 start-ups valued at US$ 75 billion and employing 300,000 people. This makes India the world’s second largest start-up ecosystem while the growth rate is estimated to be highest here.